As shopping centre markets reach maturity in most European countries, there will be growing polarisation between successful prime schemes and struggling secondary sites which are having to diversify to survive, according to new research from Cushman & Wakefield.

The firm’s annual ‘European Shopping Centre: The Development Story’ report shows that approximately 2.6 million square metres of new shopping centre space was completed in 2018, 28% below the amount added in 2017. The 2018 figure represents the lowest level of completions for 24 years and is comparable with the volumes delivered in the early 1990s when the first traditional shopping centres in Central and Eastern Europe were opening.

However, while the pace of new development has been slowing over the past five years, the total size of the European market is still growing – and now stands at 168.1m sq m – increasing shopping centre competition. As developers try to retain their market positions, they are focusing efforts on redevelopment and refurbishment projects, aimed at creating sophisticated, modern and aesthetically pleasing shopping and leisure centres.

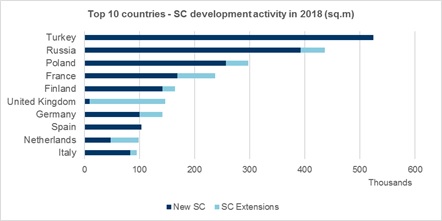

Top ten countries for new shopping centre space in 2018 (Source: Cushman & Wakefield Research)

Report author Silvia Jodlowski, Senior Research Analyst at Cushman & Wakefield, said

“Opportunities for new shopping centre development are seen mainly in two types of schemes. Dominant innovative schemes with a strong leisure element, in place of aging unattractive schemes, or smaller convenience/community retail schemes, where distance to the store, the presence of a food operator and appropriate tenant mix are crucial factors for a scheme’s success.”

Western Europe

Growing concern around the rise of e-commerce and strong growth in high street retail dampened new shopping centre development across Western Europe. France, for the fourth year, was the most active country in terms of floorspace added, with 237,000 sq m of new space to the market.

In the UK, although the ongoing shift to online has resulted in store closures, oversupply is not holding back shopping centre development. Rather than discouraging further development, it has merely focused developers’ interest in driving footfall as they strive to create unique and interactive shopping experiences via leisure extensions and mixed use developments. The UK was the third most active development market in Western Europe in 2018, with 147,000 sq m of new space delivered, of which 74% was contained in two developments. This represented an 8% rise on 2017.

In Finland, strong urban migration is supporting shopping centre development where 80% of total built space was located in the three largest regions: Helsinki, Tampere and Turku. While in Southern Europe, Spain retained its top position for shopping centre development.

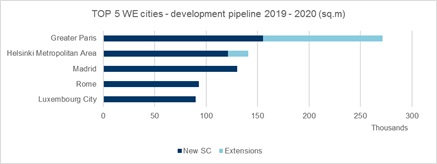

Across 2019 and 2020, 2.1 million sq m of new shopping centre space is expected in Western Europe.

Top five Western European cities for development pipeline 2019-2020 (Source: Cushman & Wakefield Research)

Central & Eastern Europe

Turkey was the most active country in Central & Eastern Europe, delivering 525,000 sq m of new space. The amount of new supply was down almost 50% on 2017, as developers begin the transition towards smaller schemes and focus on the renovation/optimization of existing centres. In Russia, the second most active European market for development activity in 2018, the volume of completions reached 436,000 sq m. While this is the lowest figure in 15 years, there is expected to be an increase in 2019/20, with 1.8 million sq m currently under construction.

The positive economic backdrop in Poland has provided a solid platform for retail development. In 2018, approximately 300,000 sq m of new space was added to the market, the third highest figure in Europe. As is the case in Western Europe, the growth of e-commerce means competition is strengthening, forcing landlords to focus on making their schemes more attractive to visitors.

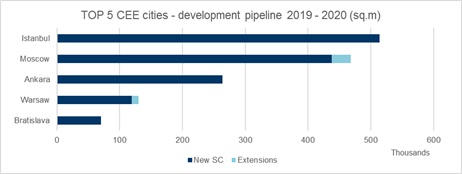

Elsewhere in Central Europe, development has been stable. In Bulgaria, the Czech Republic, Slovakia and Hungary, markets are approaching maturity. Potential new opportunities lie within mixed-use schemes, downtown areas and hubs of public transport sites. In 2019 and 2020, 4.4. million sq m of new shopping centre space is expected in Central & Eastern Europe.

Top five Central & Eastern European cities for development pipeline 2019-2020 (Source: Cushman & Wakefield Research)

Silvia Jodlowski added

“Landlords and investors will need to adapt to the polarisation of the shopping centre market. We do not expect to see much further shopping centre development in the traditional sense. In its place, we anticipate a growing number of redevelopments and reconfiguration projects to cater for the growing demand for flexible space.

“Mixed-used schemes are quickly becoming more and more popular as investors realise the true potential they hold. As we see in parts of Europe, with France being a prime example, shopping centre developers are trying to diversify with new formats such as retail parks and hybrid formats including offices, hotels and residential.”

Source: Cushman & Wakefield

Prague, June 7. 2019